There is a famous story about a couple who had a baby and came to ask the rabbi, "When should we start educating the child?"

To this question, most of us would probably answer - the age when the child begins to understand, maybe around two or three years old.

But what did the rabbi say? Too late! The process of education begins with our own personal education, and naturally, through the personal example we set, our children will learn from it and act accordingly.

The same applies to topics like buying a home and managing retirement. When we talk about buying a home, we need to ask a broader question: what is required of us to make a significant purchase or an investment in a home for residence?

Even more so with the topic of retirement, if we don't establish habits early on, we won't be able to manage properly when we reach retirement age.

How to save and why?

Naturally, at the beginning of the journey, the income of the couple is likely not very high - probably around the average income, and with God's help - as the years go by, salaries will increase.

Every day in the process of saving and investing is of great value, so it is essential and necessary to save from the very beginning. It is crucial to begin quickly, due to the importance of the time component in saving and also for developing the habit of saving early on. Even saving a small amount is better than nothing.

Where to save or set aside money?

There are five avenues:

And Rabbi Yitzḥak says: A person should always divide his money into three; he should bury one-third in the ground, invest one-third in business [bifrakmatya], and keep one-third in his possession. (Baba Metzia, 42a).

Our sages gave us good advice - divide your money so that one-third goes toward real estate, one-third is invested in a profitable business, and one-third is kept as liquid assets for daily use.

Our sages also guided us to divide our savings into different time frames - short, medium, and long-term.

In the past, there was a common saying, "Save a third without feeling it." This was an advertisement for "Haschamim," a device attached to the faucet that saves a third of the water without the user noticing the difference. The water flow continues almost the same, and you don't feel the difference in usage, but one-third of the water is saved.

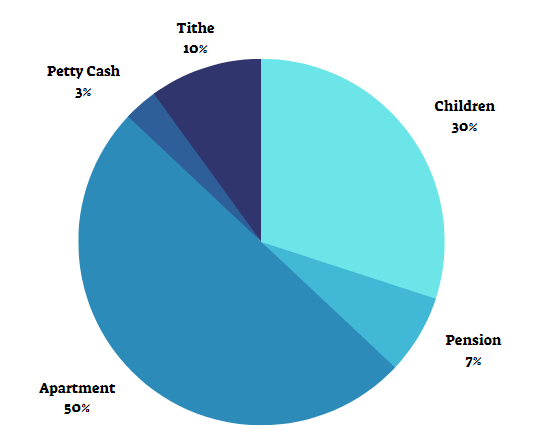

The graph relates to the internal distribution of the recommended savings.

(Further reading in my book “לחשוב מחוץ לחופה”)

Recommendation for the allocation of savings - one-third of the joint income of the couple, with half of it designated for a home.

The more we cultivate good savings habits, the closer we can get to purchasing a home and making additional investments.

It's important to remember that purchasing an apartment as an investment is not always the preferred alternative. Typically, no investment is the best but it depends on the individual's circumstances. We should always ask ourselves: “What is the alternative?”. The principle is that taking a step forward in any type of investment is better than nothing.

Seizing Opportunities at the Beginning of the Journey

As long as you don't yet have the initial amount, it's better to save and invest in high-risk assets, especially when it's a long-term investment. The time component is crucial for future returns. ("Compounded interest")

Furthermore, look for other investment opportunities, such as real estate. Parents often provide their children with an initial sum of money, allowing them to purchase a discounted property with a mortgage.

Some couples are very concerned about committing to a mortgage at the beginning of the journey. However, not purchasing a home early on could lead to missing opportunities before the significant price increases in the housing market and also losing substantial returns.

Additionally, when it comes to a ready-to-move-in property, there is a high likelihood of renting it out right from the start, which can alleviate concerns about mortgage commitments because there is a possibility that rental income will be received immediately upon purchase.

Of course, there is always a risk that no tenants will be found over an extended period. Therefore, it's advisable not to be completely dependent on rental income and strive to be in a position where there is flexibility for such situations without tenants.

Another recommendation is that when you have a rented property, allocate a budget every month from the rental income for dealing with issues under the rental agreement.

Sometimes, purchasing a property "on paper" – meaning a property that is still in the planning stage and not yet built – comes with a significant advantage. The price of the property at the time of purchase is typically lower compared to its value when it is completed, resulting in substantial returns in a relatively short period, unlike buying a ready-made property.

The drawback of purchasing at this stage is that there is no immediate rental income, meaning there is no income from tenants. Additionally, the exact date of receiving the property's keys may not be certain, despite assurances from the contractors. It's important to note that when buying a property "on paper," there is often a clause that obligates the contractor to pay rent in case of delays in handing over the property.

It is customary that for each month of delay in property delivery, the contractor is required to pay defined rental fees based on the size of the purchased property.

"Luck is what happens when preparation meets opportunity."

- Lucius Annaeus Seneca, Roman philosopher.

Proper Financial Planning for Retirement:

When it comes to saving for retirement, starting early can make a significant difference.

Dr. Lior Emsalem, a finance and capital markets specialist, suggests that even saving a few hundred shekels each month, especially when young, can lead to a substantial amount in the future due to the compounding effect.

Starting savings at a younger age allows for a relatively higher allocation to riskier assets, such as stocks both domestically and internationally through an appropriate trust fund, as the long-term return potential of risky assets tends to be higher compared to less risky investments. This approach is favored because it allows ample time to withstand market downturns.

As retirement age approaches, it is advisable to reduce the allocation to riskier assets, favoring less risky and low-risk assets like government bonds.

Dr. Emsalem provides a very wise recommendation for a couple in their early twenties. It is likely that it will take them approximately 5-7 years to establish stable and steady employment. The potential returns are heavily influenced by the time component of investment, so every month without savings is a loss.

Therefore, the recommendation is to start saving as much as possible each month, with a relatively high risk level (while considering that the future is uncertain, historical data shows a reasonable rate of return). Towards retirement age, it is advised to minimize risk, as the investment horizon becomes shorter, and the execution approaches.

As always, there are no guarantees or commitments, and it's important to be cautious of "risky" stocks and seek advice from qualified professionals.

For example, saving 500 shekels a month for 45 years at an annual interest rate of 5% (over the long term and with a relatively high-risk level) would result in approximately 1 million shekels, compared to around 270,000 shekels with no risk at all. At a 7% interest rate, the same savings would yield about 2 million shekels.

When you reach a good age for retirement, it's possible to reduce risk in initial-stage investments and assess your daily expenses and sources of income, such as a pension from work or other savings. Planning your budget and helping your children is also important.

As a recommendation – check your children's situation from time to time, and whenever possible, simply assist. The reality of life today is not simple, especially given the high cost of living. (I simply recommend giving, especially for family events, and encourage your children with kindness to enter investments.)

On a fundamental level, remember – thank God, you've reached an age where the economic burden is somewhat lighter, and your children are in the opposite situation.

Additionally, "there is no wisdom like experience," and your children need your experience. Help them with good advice or connect them with others who have experience.

"Man searches for meaning," as Viktor Frankl said. At every stage of life, we need meaning in our daily lives. Thank God, you've reached a stage where the pursuit of income or a livelihood is calming down, and it's your time for self-fulfillment while wearing your unique personality “hats”.